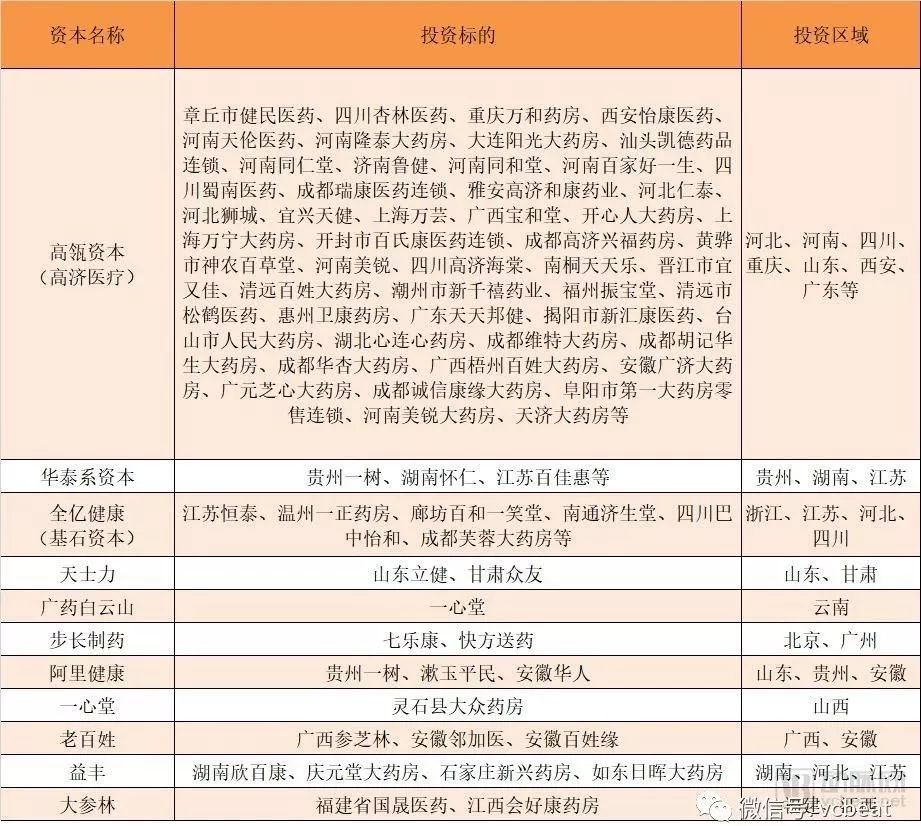

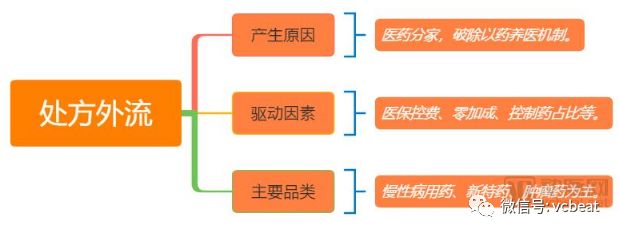

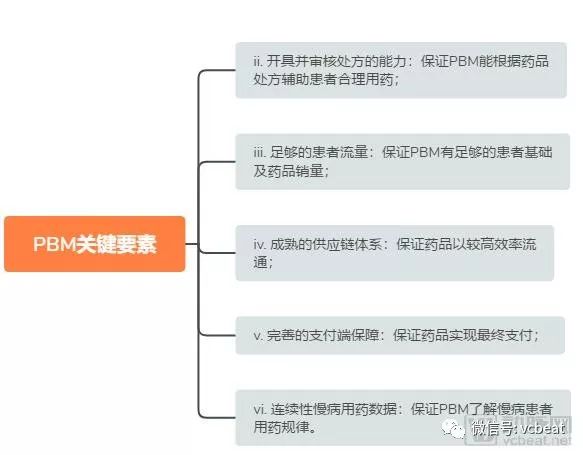

“M&A is in full swing in the first half of this year, especially the high-tech medical system of Gaoji. The rumors have been merged into tens of thousands of pharmacies, and the sales volume has reached a huge amount of 26 billion. However, the merger has started to cool down in the second half of the year, mainly these large capital consortia. The incorporation of a large number of pharmacies in the short term has led to 'digestive dysfunction' in the integration process." An industry insider told the arterial network that the trend of mergers and acquisitions in the retail pharmacy industry is changing. According to the incomplete statistics of the arterial network, in recent years, there are four major capitals that are “looking at the retail pharmaciesâ€. Including foreign capital: Gaochun Capital, Morgan Stanley and other investment institutions; pharmaceutical group: Guangzhou Pharmaceutical Baiyunshan, Tasly Group, Buchang Pharmaceutical and other industrial enterprise groups; listed chain: Yixintang, ordinary people, Yifeng, Dashenlin Internet + medical platform: Ping An, Ali, Jingdong and so on. Capital is like a catalyst for industry development. It can accelerate the process of industry evolution. The scale changes, pattern changes, and business changes that took place in a decade or even 20 years have been initially completed in just one or two years. After being quickly “cookedâ€, the problems that mergers and acquisitions and traders in the retail pharmacy industry should think about are how to avoid “complete and inconsistentâ€, how to quickly bring out the scale effect, and even exceed the expected value return. After all, the most important thing in business is the forward-looking and strategic advancement of strategy. This article mainly discusses the problems of the chain pharmacies “the era after mergers and acquisitionsâ€. The structure is as follows: 1. From “value investment†to “complete and inconsistentâ€; 2. The outflow of prescriptions is less than expected, and the impact of “Internet + medicineâ€; 3. Does the US's vertical integration model have reference value - commercial insurance, PBM; 4. Pharmacy classification management - the greater the ability and the greater the responsibility. From "value investment" to "complete and inconsistent" There is no doubt that mergers and acquisitions in the chain pharmacy industry have begun to cool down. There are several appearances of this trend. One is price, that is, as the trend of mergers and acquisitions develops, the price of mergers and acquisitions is getting higher and higher, and it has reached the critical point. The second is the standard, with the big capital, the big consortium, the capital of the industry. Enclosure, high-quality, scarce standards have become a thing of the past; the third is the "negative effect of scale". With the increase in the size of chain pharmacies in capital management, the original manpower reserve, organizational structure, and management methods are insufficient to control the scale of enterprises. The friction costs in the enterprise are getting higher and higher. Capital "hunting" chain pharmacy Source: Arterial Network Below we split each by one. The first is the price, the chain pharmacy industry M&A integration mainly has two price evaluation models - price-earnings ratio, market-to-sales ratio, generally measured by the market-to-sales ratio, that is, the M&A price divided by the pharmacy's annual sales. The market for pharmacy mergers and acquisitions has been bullish all the way. Two years ago, this value was 0.7-0.9 times, but many of them have already risen more than one time, like the courtyard stores and big stores. Up to 1.5 times. Don't underestimate this change. The average annual income of a pharmacy is 2 million. If the company that is funded has 200 stores, according to the previous valuation method, the price is about 300 million, and the market is 1.5 times. The calculation will cost 600 million yuan, and the price will soar. It will be more difficult to deal with the capital winter. In addition, many of the mergers and acquisitions of capital participation in retail pharmacies are listed on the listed companies in the industry, such as Yixintang, ordinary people, etc. Listed companies look at the price-earnings ratio. In principle, the price-earnings ratio of the acquired companies will definitely not be higher than that of listed companies. To go to the market, it also needs a series of processes such as restructuring, restructuring, optimizing operations, and listing counseling, that is, “the price of flour is lower than breadâ€. However, the stock market has recently suffered setbacks, and the market value of many retail pharmacy concept stocks has been adjusted back. At this time, investing in the secondary market is more favorable than investing in the primary market, resulting in bread being cheaper than flour and the valuation level is seriously upside down. Let us look at the standard situation in the market. Capital will definitely not find a company with too small scale. It is generally a city-level leader, the so-called “growth†pharmacy, which may become the leader of regional chain pharmacies. The sense of smell of capital is very keen. Under the tireless digging of everyone, many high-quality targets have already been "famous." In fact, industry insiders judge that more than 80% of regional leading enterprises are introducing the power of capital in the process, and it is the power of capital that helps it to integrate regionally, and then has the power beyond its own hematopoietic development. There is not much left in the quality standard, and the rest is either the price is too high, or the company itself has no intention to introduce capital, and it is not suitable for large-scale injection of capital. Finally, the “negative effect of scaleâ€, the original words of the industry: tens of thousands of pharmacies integrated, involving hundreds of acquired companies, this management is unprecedented. After the company is acquired, the original founders will often choose to cash out or retreat to the second line. The original resource advantages and execution will be greatly reduced. The acquirer will strengthen management ability and improve operational capability. Otherwise, the decline in the performance of the acquired company is inevitable. . Capital injection is like organ transplantation. It also has rejection. If you want to reduce rejection, you need to do immunosuppression. The result of immunosuppression is short-term performance adjustment. To a large extent, this adjustment is inevitable. So summed up the trend of M&A in the chain pharmacy industry: the quality of the standard is less, the price is getting higher and higher, from the perspective of financial investment, there is a better investment target, and after the high-speed merger, a digestive process is needed. Both lead to the arrival of the industry's M&A integration turning point, and the industry will enter the “post-merger eraâ€. Prescription outflows are less than expected, "Internet + medicine" shock To a large extent, capital entering the retail pharmacy industry is "gambling" in the future. Capital is optimistic about pharmaceutical retail mainly for three reasons: First, pharmaceutical retail is not a high barrier, it is easier to enter; second, the concentration of domestic pharmaceutical retail industry is very low, capital intervention helps industry consolidation; It is a policy that favors the development of retail pharmacies, such as the liberalization of medical insurance qualifications and the opportunity for prescription outflows under the separation of medicines. The focus of capital is on the third point, especially the opportunity for prescription outflows under the separation of medicines. From the perspective of global experience, the separation of medicines is an inevitable trend. The United States adopts a more thorough separation of medicines, and about 60-70% of medicines pass. Non-hospital channel sales (pharmacy, PBM mail order); Japan has been practicing medicine for more than 40 years, and currently about 70% of prescription drugs are sold outside the hospital. The experience of the United States and Japan provides a certain reference for us to measure the scale of domestic prescription outflows. Some institutions predict that this scale will reach trillions. For retail pharmacies, this is a brand new incremental market, and the room for growth in performance is self-evident. But think carefully, the prescription outflow does not constitute a new business model element, it is not like the e-commerce changes to the retail business, only by the habits of consumers and suppliers can be achieved. The implementation of prescription outflow is very complicated, and there are many participants, including social security, health care, drug supervision, hospitals, doctors, pharmacies, etc. Any one of the links says “no†to the prescription outflow, and this matter will be largely stranded. Relatively speaking, the pharmacy is the recipient in the outflow of prescriptions. It is the passive side. It can only wait for the policy to be approved and the hospital to transfer the prescription. The pharmacy is weak in controlling the entire process of prescription outflow. Retail pharmacies want to take over the prescription outflow, and they must cross the “three big mountainsâ€: the source of prescriptions. Generally speaking, few retail pharmacies have strong connections with hospitals – except for wholesale and retail enterprises. Conversely, distribution and distribution enterprises have hospital resources. It is able to get prescriptions; secondly, the ability to supply medicines and pharmacy services. In the long run, prescription drugs are not the focus of pharmacies, nor are they the primary source of profits, so pharmacies have limited prescription drugs and service capabilities; With the support of social security, it is difficult to get through the social security co-ordination. If it is not reimbursed, the ability to attract patients is limited. Of course, this is not to say that retail pharmacies can not accept prescription outflows at all, but only that if retail pharmacies want to undertake prescription outflows, they may have lower expectations due to their own business characteristics and management methods. The problems are all found out, the next step is how to overcome, this is also the focus of the "post-merger era" management. In addition, we should talk about the impact of the “Internet + Medicine†model. One is the impact of capital level, such as Ping An, Ali, JD.com, etc. In the pharmaceutical retail sector, Ali is the most integrated system, and it uses the “health flagship platform†of big health. In the near future, Ali Health has intensively invested in the regional leading chain pharmacies such as Shandong Yuyu civilians, Anhui Chinese health, and Guizhou Yishu. In the area where these chain pharmacies are located, the integration of online and offline pharmaceutical retail channels is promoted. Ali’s shareholding is a relatively The “moderate†shareholding does not seek absolute control, nor does it require performance against gambling. This is a very good opportunity for regional leaders who want to be big. The second impact of the "Internet + Medicine" model is "new retail" - or O2O, why is the O2O model a shock to the traditional retail retail model? Because the traditional retail pharmacy is doing a business of 300-500 meters, it is a pure-line business. In a good position, with a good flow of people, there will be good development. O2O enhances the coverage of individual pharmacies and can carry out 3-5 kilometers of radiation. The most intuitive effect is that pharmacies should not be so much, the number of pharmacies in one area will be greatly reduced, and many pharmacies that fail to meet expectations will definitely Be eliminated. The impact of O2O on traditional pharmacies is also reflected in the decrease in the number of people entering the store. The original purchase of drugs must go to the store. After the store is available, the store staff can conduct secondary development after purchasing, recommending and perfecting the information sheet, such as membership management. Promotions, etc. However, in the O2O mode, you don't need to go to the store to buy medicines, there is no way to recommend them, and there is no way to carry out secondary development. This allows consumers to completely detach from the pharmacy's control, and many of the original online marketing can be completed. The activity online became an unknown number. The correct way to open in the future should be to guide the line to the line, to guide the line to the line, to guide each other under the line, and to blur the line between the line and the line. In addition, explore more geographically based new medical retails based on medical consumption big data. In this regard, Ali, JD, and the US Mission are pioneers and have experience, and early participants in the industry will also benefit. Does the US's vertical integration model have reference value? Commercial Insurance, PBM Another big event in the global pharmaceutical retail industry recently is that the US pharmacy star company CVS announced the completion of the acquisition of health insurance company Aetna (Antai), a $69 billion deal announced in December 2017, which is not only the US pharmaceutical retail industry. The biggest deal in history was the biggest merger and acquisition event in the global pharmaceutical industry in 2017. The US pharmaceutical retail industry is now in a double-matched situation. CVS is slightly less than Walgreens in terms of store number and retail size, but overall revenue exceeds Walgreens. According to the CVS 2016 annual report, it has more than 9,700 pharmacies in the United States, of which 1,100 are equipped with “minute clinics†and PBM business (pharmaceutical welfare management) has nearly 90 million members. In 2016, CVS revenue was $177.526 billion, up 15.8% from 2016; net profit was $5.319 billion, up 1.5% from 2015. Aetna is one of the oldest health insurance companies in the world. In 1850, the Annuity department was opened and the life insurance business was started. In 1853, the Annuity department independently established Antai Life Insurance Company. In the United States, the company is at the forefront of the medical, dental, pharmaceutical, and life and group disability insurance industries. According to Aetna's 2016 annual report, its 2016 revenue was US$63.155 billion, up 5% from 2015; net profit was US$2.271 billion, down 5% from the previous year. Also according to the Aetna 2016 Annual Report, it has 23.11 million health insurance members. The combination of pharmaceutical retail and commercial insurance is in the PBM business. After CVS will receive Aetna, it will form a health service system covering “PBM+Pharmaceutical Retail+Health Insurance+Medical Servicesâ€. Aetna's 23 million members will become CVS's “flowâ€. Source, and Aetna will also enjoy the finer drug benefits management and fees provided by CVS. More importantly, the combination of the two will form a strong bargaining alliance, and the bargaining power of pharmaceutical companies and medical institutions will be stronger, which will help further reduce operating costs. In fact, it is the PBM business that helped CVS run out of the “second growth curveâ€. This has been clarified in the previous CVS case analysis of the arterial network: from the CVS business model, the entire group is divided into two major groups. The core department is the pharmacy service department and the retail department. The essence of pharmacy services is to earn management fees and other related expenses by signing agency contracts with institutions/enterprises; the essence of the retail sector is to make profits through online and offline sales. These two departments have shown a certain degree of cross-sectoral business in recent years as the business line continues to expand. These two departments constitute almost all of CVS's revenue. The pharmaceutical welfare management model PBM, known as Pharmacy Benefit Management, refers to a specialized third-party service. The PBM model is mainly a management coordination mechanism between insurance institutions/welfare institutions, pharmaceutical companies, patients and pharmacies. It is established to effectively manage medical expenses and increase the cost of medical treatment while saving the payment. The benefits of the demand side. Key elements of PBM Source: Yikai Capital The core of the US PBM model is to penetrate all aspects of pharmaceutical circulation, and to balance the interests of the parties such as the payer, supplier, channel and demand side through contract signing. PBM agencies develop a catalogue of prescriptions through their powerful database to provide more cost-effective prescription drugs based on the drug needs of different clients. The medical expenses of the payer are reduced while ensuring high quality treatment for the patient. The main role of the PBM model in the entire pharmaceutical circulation is: 1) Establish a database through a large number of clinical data and historical data on the use of insured persons, and conduct a reasonable review of the prescriptions issued by doctors; 2) Regulating the use of drugs in patients, controlling the phenomenon of excessive medical treatment and drug abuse; 3) Utilize the advantages of its own users, through the high bargaining power of pharmacies and pharmaceutical companies, sign contracts to effectively control the cost of prescription drugs; 4) Reduce insurance expenses and realize medical control fees; 5) Connected with multi-stakeholders (mainly patients, insurance institutions, pharmacies and pharmaceutical companies) in the pharmaceutical distribution industry, and achieved multi-party resource integration; Many retail pharmacies in China have indicated on different occasions that they should learn from CVS's development experience and benchmark against CVS, but few companies can combine the pharmaceutical retail business with the PBM business. Of course, the reason behind this is very complicated, involving the difference between the payment of medical expenses - the United States is mainly commercial insurance, China is mainly social security, and the social security control model is an administrative appeal, far from the market; As well as the degree of retail scale, the US medicines are separated earlier, and the retail pharmacy industry is more obvious. CVS, Walgreens, ESI and so on occupy an absolute leading position in retail, and also facilitate drug services within the group and industry. , medicine + insurance services. However, the US pharmaceutical retail enterprises carry out cross-industry and vertical integration in the pharmaceutical industry chain, which is also valuable for Chinese retail enterprises. When horizontal integration encounters the ceiling or reaches the inflection point, vertical integration can not only break the deadlock, but also often achieve unexpected breakthroughs. The difference or advantage of China's retail pharmacy business compared with the US is that our pharmacy is highly saturated, the pharmacy service has a small per capita population, and there is time and space to provide more innovative services. In addition, the pharmacy coverage is very high. In the urban area, there must be a pharmacy within 300-500 meters. The pharmacy is a natural health service unit at the doorstep. It is closer to the end users and has the potential for intimate service. It also has a high level of urbanization and concentrated living. These are all advantages. How to convert depends on whether the industry can make good use of these resources. In fact, we are currently seeing “retail +†innovations in the domestic pharmaceutical retail industry, such as “retail + insuranceâ€, “retail + e-commerceâ€, “retail + medical servicesâ€, “retail + health managementâ€, etc. The model is still in its early stages, but in time, it can highlight the value of innovation. Pharmacy classification management - the greater the ability, the greater the responsibility On November 23, the Ministry of Commerce issued a notice on the public consultation for the “Guidelines for the Classification and Classification Management of National Retail Pharmacies (Draft for Comment)â€. The drafting instructions of the notice pointed out that in recent years, China's pharmaceutical retail market has shown a development trend of stable growth, structural optimization and quality upgrading. Statistics show that in 2017, the national pharmaceutical retail market sales totaled 400.3 billion yuan, an increase of 9.0%. There were 5,409 pharmaceutical retail chains and 454,000 retail pharmacies. However, at present, the problem of “small, scattered and chaotic†in the pharmaceutical retail industry is still outstanding. The level of industry standardization, informatization and intensification is generally low, and the management level and service capacity of pharmacies are uneven, which restricts the sales of prescription drugs and the management of drug services. The role played. In some areas, the layout of retail pharmacy outlets is not balanced. In some remote areas, the supply of medicines in pharmacies is insufficient. There are problems such as inconvenient and uneconomical purchase of medicines by patients. The role of industry services in health is not yet fully realized. There is a big gap between the overall development level of the industry and the reform requirements of medical, medical insurance and medical “three medical linkagesâ€. It is difficult to support the implementation of various key reform tasks such as grading diagnosis and treatment, modern hospital management, universal medical insurance, drug supply security, and comprehensive supervision. Promoting the classification and management of retail pharmacies is conducive to accelerating the process of transformation and upgrading of the pharmaceutical retail industry, and is conducive to creating basic conditions for deepening the "three medical" linkage reform, which is conducive to the improvement of management level by industry management departments and enterprises, and is conducive to patients' access to economics and convenience. Quality medicines and services, creating a good environment for purchasing medicines. We believe that the core logic of pharmacy classification and grading management is “the greater the capacity, the greater the responsibilityâ€. Why do you say this? Because retail pharmacies are divided into three categories according to operating conditions and compliance: one type of pharmacy can operate Category B. Non-prescription drugs; second-class pharmacies can operate non-prescription drugs, prescription drugs (excluding prohibited, restricted drugs), Chinese medicine decoction pieces; three types of pharmacies can operate non-prescription drugs, prescription drugs (excluding prohibited drugs), Chinese medicine decoction pieces. Operating conditions and compliance status include the quality assurance capabilities of pharmaceutical pharmacies, the configuration of pharmaceutical technicians, and administrative penalties. This means that the pharmacies that already have advantages will be tilted by the resources of the administrative license, and the space for development will become larger and larger. Of course, rights and obligations are also matched. To achieve high-level pharmacy standards, the initial investment will be increased accordingly. When the cost recovery cycle of new pharmacies is lengthened, it will promote the integration of pharmacy industry stocks, and it will also benefit mergers and acquisitions within the industry. Business upgrade. Opportunities and challenges coexist, and retail pharmacies took off at the right time. For future industry trends, we have the following pre-judgment: 1. Capital enters the pharmaceutical retail industry to usher in an inflection point, paying more attention to the balance of price and future value; 2. After a large-scale merger and acquisition, there will be a certain adjustment period, and the performance will return briefly; 3. M&A integration will increase industry concentration, and the future industry pattern may be several national leaders + several regional leaders; 4. The separation of medicines will continue to be implemented, and retail pharmacies will become one of the recipients of prescription outflows; 5. DTP pharmacies and professional pharmacies have developed rapidly and become important formats independent of general chain pharmacies; 6. The “Internet + Medicine†model continues to infiltrate, and new retail and O2O models are sweeping across the country; 7. Retail pharmacies will be integrated with Internet medical, medical e-commerce, O2O and other modes. The whole channel will become the norm in the industry. The member management and operation capabilities will help the market to compete and create entrepreneurial opportunities. 8. Pharmaceutical retail enterprises began to vertically integrate and strengthen cooperation with commercial insurance and health management companies, and the “retail +†model innovation increased; 9. The cost of new construction of retail pharmacies has increased, and the barriers to entry have increased, which will help to further stock integration.

Chinese herbs have a long history, and we have thousands of years of experience and methods of using herbs. There are countless precious herbs on the land of China, which play a vital role in human life and health. High quality raw materials will benefit more people in today's world driven by modern science and technology. By adopting new modern high technology, the manufacturers extract and purify the essence of the valuable herbs to let more people could benifit it.

Natural herbs, originating from nature, are healthier and more assured. The herb extracts are very excellent raw materials for the health care products.

Our company, Allied, provides various herbal extracts, including ginger extract, pueraria root extract, black wolfberry extract, Angelica root extract, moringa leaf extract, honeysuckle extract, rhodiola rosea extract, Astragalus membranaceus extract, paeony root extract, black garlic powder, matcha powder, etc.

Besides the raw materials, we are also able to custom your own formula upon your unique requirements.

Natural healthy Herb Extracts, Health care product raw materials, black wolfberry extract Allied Extracts Solutions , https://www.alliedbiosolutions.com